Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Don’t let this market scare you and don’t make every up-at-bat a strike-out. Join me as I walkthrough a simulated multiple offer situation to understand the factors a seller looks at, why certain elements are important and how they land on a “best” offer. Email me at harrisonrealtyteam@gmail.com to get the link to the webinar. Can’t attend? No problem! Still email me and I’ll be sure to send you the recording.

Don’t let this market scare you and don’t make every up-at-bat a strike-out. Join me as I walkthrough a simulated multiple offer situation to understand the factors a seller looks at, why certain elements are important and how they land on a “best” offer. Email me at harrisonrealtyteam@gmail.com to get the link to the webinar. Can’t attend? No problem! Still email me and I’ll be sure to send you the recording.

Uncategorized •

June 18, 2025

Slide Into Home This Summer!

Uncategorized •

June 18, 2025

CB’s Tips for Increasing Value with a Basement Remodel

Thinking of remodeling your basement? It can be a great tool in adding space and property value, but there are some factors to consider. Coldwell Banker walks you through 6 steps to maximizing your basement’s potential.

Uncategorized •

March 23, 2025

CB’s Tips For Sprucing Up Small Outdoor Space

Want to take advantage of the great weather being ushered in but are struggling with how to utilize the small amount of outdoor space you have? Even the smallest of outdoor spaces can be transformed into welcoming, functional outdoor retreats with these tips from Coldwell Banker! Find CB’s tips here!

Want to take advantage of the great weather being ushered in but are struggling with how to utilize the small amount of outdoor space you have? Even the smallest of outdoor spaces can be transformed into welcoming, functional outdoor retreats with these tips from Coldwell Banker! Find CB’s tips here!

Uncategorized •

March 23, 2025

Spring Home TLC Guide

Get ready to shake off the winter blues and give your home the TLC it deserves this Spring!

Spring welcomes the perfect opportunity to step outside and elevate your home’s curb appeal. The in-between period as winter shifts to spring can be tricky, so here are a couple of things we recommend doing to maximize your curb appeal & property value:

Undo the Winter Damage!

Undo the Winter Damage!

✅ Clean Up: Remove dead leaves, branches, and debris from your lawn and garden beds.

✅ Trim & Prune: Shape bushes and trees to promote healthy growth and improve visibility.

✅ Mulch: Add a fresh layer of mulch around plants to help retain moisture and give your landscape a polished look.

Let the Sun Shine!

✅ Clean your windows: Deep clean your windows to not only refresh their exterior look but also let natural light flood into your home

✅ Refresh Your Paint: Paint any peeling paint or add another coat to being new life into your home’s exterior

✅ Color: Add pops of color through elements like flowers and vibrant doormats and wreaths

✅ Power Wash: Clean your driveway, sidewalks, and siding to remove dirt and grime.

Uncategorized •

February 18, 2025

CB’s Tips for Touring Homes Like a Prop

A Buyer’s Checklist for Touring Homes!

Home tours are one of the first steps in purchasing a home and a vital one. However, what should you look for? Being prepared will give you the confidence you need to focus on the most crucial aspects and make the right decision on moving forward. Find out all of Coldwell Banker’s tips for touring homes like a pro here: https://blog.coldwellbanker.com/a-buyers-checklist-tour-homes-like-a-pro/

Uncategorized •

February 18, 2025

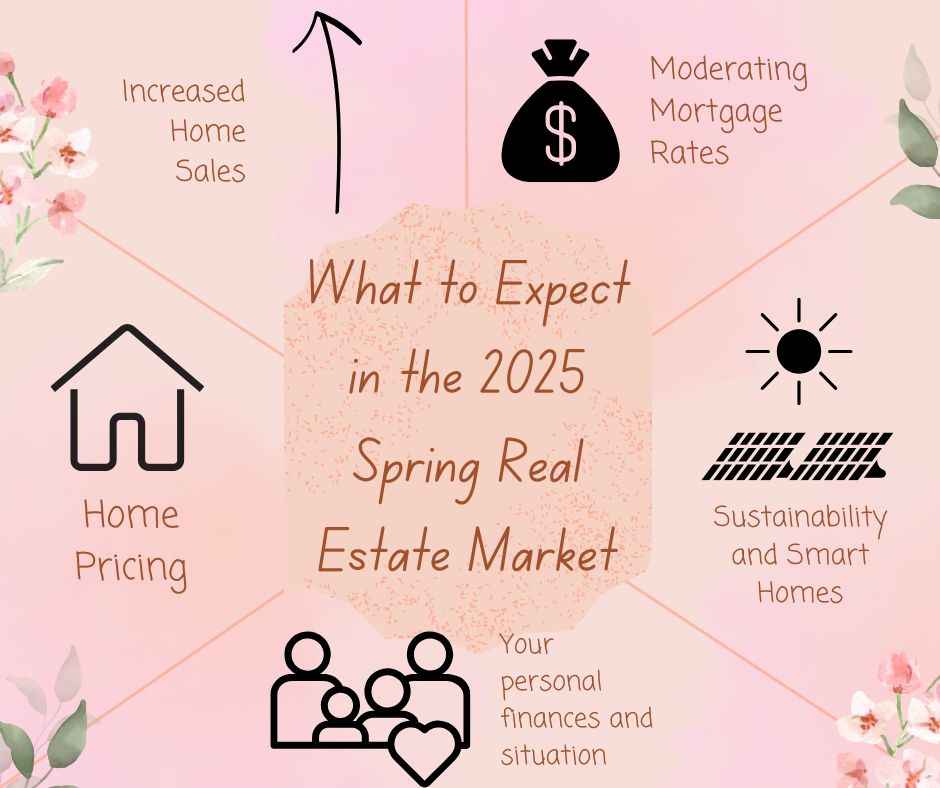

What To Expect in the 2025 Spring Real Estate Market

What to Expect in the 2025 Spring Real Estate Market

As we approach the spring of 2025, the real estate market is poised for some interesting developments. Whether you’re a potential homebuyer, seller, or investor, understanding the trends and predictions can help you navigate the market more effectively. Here’s what you can expect:

homebuyer, seller, or investor, understanding the trends and predictions can help you navigate the market more effectively. Here’s what you can expect:

1. Moderating Mortgage Rates

Mortgage rates have been a significant factor in the housing market over the past few years. For 2025, experts predict that mortgage rates will hover between 6% and 7%. While these rates are higher than pre-pandemic levels, they are expected to stabilize, providing some relief to buyers who have been grappling with affordability issues.

2. Increased Home Sales

The National Association of REALTORS® forecasts a rise in home sales for 2025. Existing home sales are expected to increase by 9%, while new home sales could jump by 11%. This uptick is driven by improving job numbers and a growing economy, which are motivating more Americans to enter the housing market.

3. Price Deceleration

After years of rapid price increases, the pace of home price growth is expected to slow down. This deceleration is partly due to increasing inventory and softer demand as buyers adjust to higher mortgage rates. While prices will still be high, the slower growth rate could make homes more accessible to a broader range of buyers.

4. Shift in Buyer Demographics

The demographics of homebuyers are changing. There’s a notable increase in all-cash buyers, multigenerational purchases, and single buyers. These shifts reflect broader societal trends, such as aging populations and changing family structures, which are influencing the types of homes people are looking for.

5. Sustainability and Smart Homes

Sustainability continues to be a significant trend in the real estate market. Homebuyers are increasingly looking for energy-efficient homes with smart technology. This trend is expected to grow as more people become conscious of their environmental impact and seek homes that offer long-term savings on utilities.

6. Your Life and Your Advocate

Despite the uncertainty in the housing market, you can still make informed decisions by considering expert opinions. However, never let market predictions dictate your housing choices. Your personal situation and finances should always take precedence. Life happens, and if you need to make a move that’s best for you, ensure you hire a Realtor who can guide you with your best interests in mind. Find your advocate.

Conclusion

The 2025 spring real estate market is shaping up to be dynamic and multifaceted. With moderating mortgage rates, increased home sales, and a shift in buyer demographics, there are opportunities and challenges for everyone involved. Staying informed about these trends can help you make better decisions, whether you’re buying, selling, or investing in real estate.

Uncategorized •

January 16, 2025

Coldwell Banker’s 7 Upgrades for 2025

Coldwell Banker has created a list of the top 7 upgrades to your home in 2025 that will not only elevate your home’s value, but also your quality of living. They think this should be a top priority for 2025, considering the current market:

Hint: Bathroom Renovations may be 1 of their suggestions

“Since the housing market is expected to remain competitive, it’s more important than ever to consider improvements.”

Uncategorized •

January 16, 2025

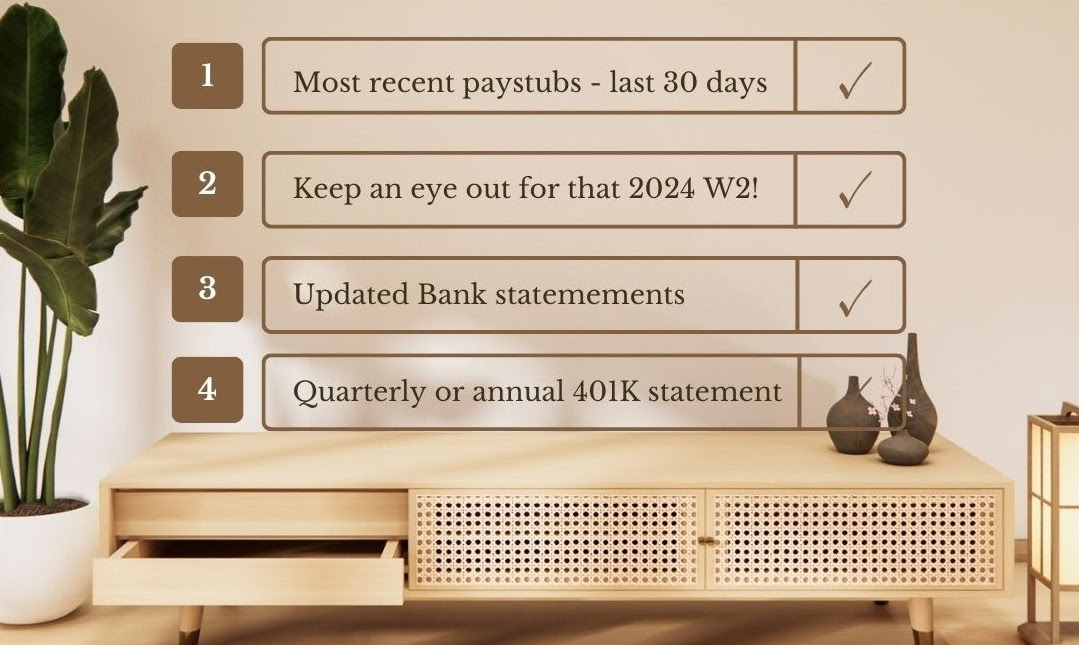

New Year….New Preapproval

Refreshing your mortgage preapproval is a good idea if it’s been a while since you initially applied, or if there have been any significant changes to your financial situation.

To help you with this task, I’ve partnered with Mandy Miller of First World Mortgage to compile of list of what you’ll need to do to get the ball rolling:

Mandy Miller

Senior Mortgage Advisor

First World Mortgage

Cell: 203-530-4361

Email: mandy@firstworld.com

- 📅Confirm Your Preapproval Expiration Date. Preapprovals usually last between 60 and 90 days. If it’s been longer than that, you may need to go through a new round of verification, especially if major life changes have occurred.

- 📞Contact Your Lender or Broker. Reach out to the lender or mortgage broker you worked with before, or consider contacting a new one if you’re exploring options. Let them know you’d like to update your preapproval.

- 💰Review Your Budget & Mortgage Goals. If your circumstances have changed—whether it’s an increase in your income, a shift in your down payment savings, or an updated goal for your home purchase—let the lender know so they can adjust their guidance.

- 📈Revisit Your Credit Score. If you’ve made any changes to your credit, like paying down credit cards or resolving disputes, this could positively impact your preapproval. On the other hand, if your credit has taken a hit, be prepared for that to affect the preapproval amount or interest rate.

- 📄Provide Updated Financial Documentation. Lenders will need to reassess your current financial situation. This usually includes:

- Recent Pay Stubs: Typically, the last 2–3 pay periods.

- Tax Returns: The last two years of tax returns, including any W-2 or 1099 forms. **keep on the lookout for 2024 W2’s!

- Bank Statements: Most recent 2–3 months of statements from all accounts (checking, savings, etc.).

Once you provide the updated information, the lender will reassess your situation and provide you with a new preapproval letter. This updated letter will allow you to confidently make offers on homes, knowing you’re ready for financing!

{kind=link}